Credit scores play a central role in modern personal finance, influencing everything from loan approvals and interest rates to rental applications and insurance premiums. Despite their importance, credit scores are often misunderstood. Understanding how they work—and how to improve them—can lead to better financial opportunities and long-term stability.

What Is a Credit Score?

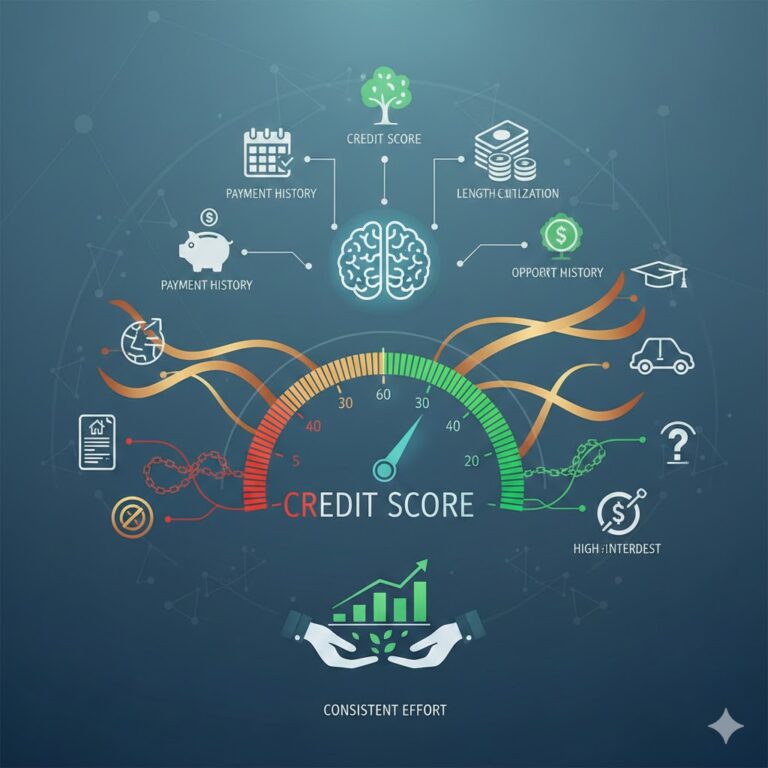

A credit score is a numerical representation of a person’s creditworthiness, based on their financial behavior. Lenders use credit scores to assess the risk of lending money. While scoring models vary, most credit scores are influenced by the same core factors: payment history, credit utilization, length of credit history, types of credit, and recent credit inquiries.

Payment history typically carries the most weight. Consistently paying bills on time demonstrates reliability, while late or missed payments can significantly lower a score. Credit utilization refers to how much of your available credit you are using. Lower utilization generally signals better financial management.

Why Credit Scores Matter

A strong credit score can result in lower interest rates, higher credit limits, and easier approval for mortgages, car loans, and credit cards. Conversely, a poor credit score can limit access to credit or increase borrowing costs. In some cases, employers and landlords may also review credit reports as part of their decision-making process.

Credit scores are not static. They change over time based on financial behavior, which means improvement is always possible with consistent effort.

Practical Ways to Improve Your Credit Score

One of the most effective ways to improve your credit score is to pay all bills on time, every time. Even a single late payment can have a lasting impact. Setting up automatic payments or reminders can help maintain consistency.

Reducing credit card balances is another key strategy. Keeping your credit utilization below 30 percent—and ideally lower—can positively influence your score. Avoid closing old accounts unless necessary, as longer credit history generally benefits your score.

Limiting new credit applications also helps. Multiple hard inquiries in a short period can signal financial stress and temporarily lower your score. Instead, apply for new credit only when necessary and strategically.

Monitoring and Maintaining Your Credit

Regularly checking your credit report allows you to track progress and identify errors that could negatively affect your score. Incorrect information can and should be disputed, as it may unfairly lower your credit rating.

Improving a credit score is not about quick fixes. It requires disciplined financial habits and patience. Over time, responsible credit management leads to stronger scores and greater financial flexibility.

Understanding credit scores empowers individuals to make smarter financial decisions. With awareness and consistent action, improving your credit profile becomes an achievable and worthwhile goal.

No comments